Scroll down for the revision notes!

1.0 Foundations of Economics

Scarcity:

- Scarcity exists due to finite resources (land, labour,

capital and enterprise) but infinite wants

- As a result, consumers, firms and governments have to constantly make choices

- Choice – people have limited incomes/ financial resources so we need to choose between alternatives, incurring opportunity cost

- Opportunity cost – the next best alternative foregone when

an economic decision is made

- Must be an economic good and is not expressed in monetary terms

The basic economic problem:

- The above choices

are often expressed as three questions that represent the basic economic

problem:

- What should be produced and in what quantities?

- How should it be produced?

- For whom should it be produced for?

Rationing systems: planned economies vs free market economies

- Planned economy: economic decisions such as what to produce, how to produce and who to produce for are made by the government

- All resources are collectively owned – governments arrange all production, set wages and set prices through central planning

- Total production, investment and consumption are often too complicated to plan efficiently even in a small economy – misallocation of resource

- Little incentive to work, less freedom of choice

- Free market (capitalism): producers and consumers do as they like without government via the price mechanisms (Adam Smith’s theory of the ‘invisible hand’)

- All production is in private hands and demand and supply are left free to set wages and prices in the economy

- Demerit goods may be over-provided, while merit goods will be underprovided

In reality, economies are a combination of the two, so mixed economies. Only the degree of the mix varies from country to country, ex. China is more of a planned economy than the UK.

Positive vs normative economics

- Positive economics deals with description and factual analysis that can be proven to be right or wrong

- Normative is a matter of opinion and is open to personal opinion and belief

Factors of production: are the scarce resources that an economy has at its disposal to produce goods and services

- Land: represents all natural resources (physical land, raw materials)

- Labour: physical and mental contribution of existing workforce to production

- Capital: investment that leads to production go goods and services

- Physical capital – stock of manufactured resources like factories, machinery

- Human capital – value of workforce (education, improved healthcare)

- Social overhead capital- large scale public system, services, facilities of a country, infrastructure

- Enterprise/ management: organisation and risk taking factor in organising the other factors of production

- Organise the other factors of production and use their personal money and that of investors to produce goods and service

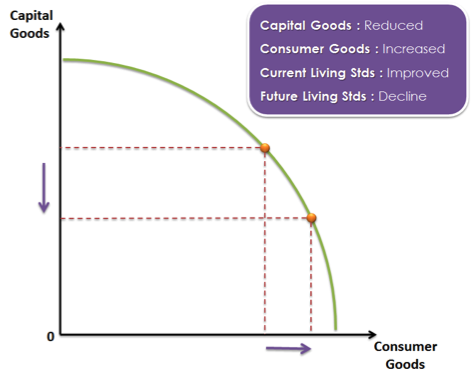

Production Possibilities Curve (PPC)

- PCC: shows the

combinations of two goods/ services that can be produced efficiently with a

given set of resources – the potential output

- Scarcity does not let the economy produced outside of the PPC

- the economy has to make choices about the combination of goods it wishes to make, resulting in opportunity cost

- PPC is curve because as more consumer goods are produced, more capital goods have to be given up – increase in opportunity cost due to law of diminishing returns

- A shift in

the PPC represents an improvement (or reduction) in productivity, efficiency and potential output

- Increase in quantity or quality of factors of production

- new and improved technology

- warfare or disease

Utility

- Utility:a measure of

the usefulness and pleasure a consumers receives when they consume a product

- Total utility: total satisfaction gained from consuming a certain quantity of product

- Marginal utility: extra utility gained from consuming one more unit of a product – usually falls as consumption increases

Revision Notes:

Useful links: